Home equity loan: What is it & how does it work?

Table of Content

Keep in mind that lenders usually offer better rates to borrowers who opt for shorter terms. Even though home equity loans have lower interest rates, your term on the new loan could be longer than that of your existing debts. A home equity loan—also known as an equity loan, home equity installment loan, or second mortgage—is a type of consumer debt. Home equity loans allow homeowners to borrow against the equity in their homes. The loan amount is based on the difference between the home’s current market value and the homeowner’s mortgage balance due. Home equity loans tend to be fixed-rate, while the typical alternative, home equity lines of credit , generally have variable rates.

If you only make these minimum payments, you won’t make any progress in paying the principal. Home equity loans can be attractive options if borrowers are seeking a lump sum of cash upfront. With a second mortgage, you might be able to use the equity you’ve accrued to improve your living space and increase your home’s value.

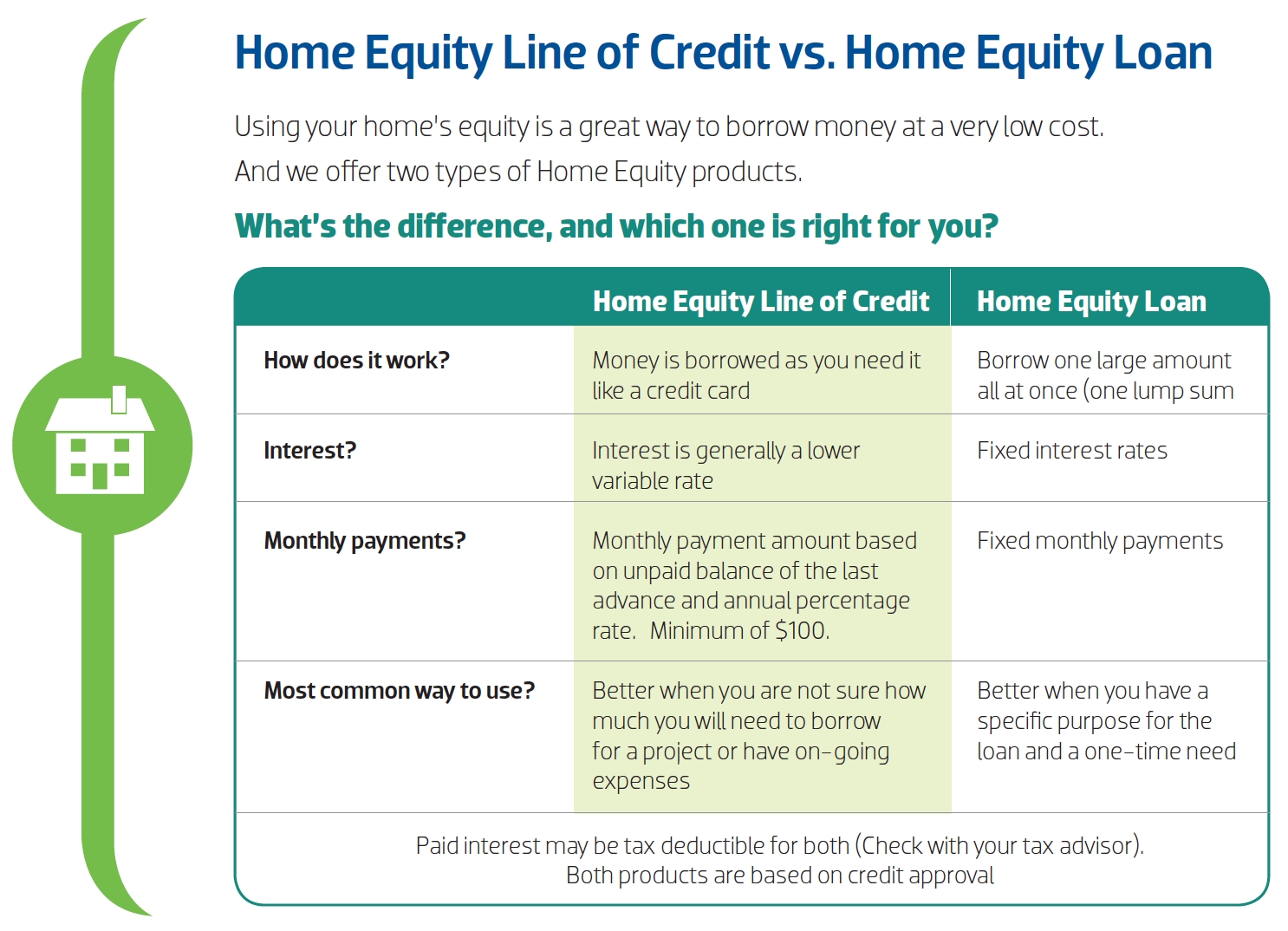

What Are Home Equity Loans and HELOCs?

Before you sign a loan, make sure you're really only borrowing the amount you need, and aren't borrowing extra. The two most common types of home loans are home equity loans and HELOCs. Starting a business is a risky venture, so you need to think carefully about leveraging your home to build one. You’ll at least have some peace of mind knowing your interest rate won’t change based on the housing market—unless you get a variable-rate HELOC.

Selling allows you to cash out all of your equity and use it however you want. Some people buy a less expensive home to start out, then sell to upgrade when their finances are stronger. The equity you accumulate through years of homeownership can become the down payment for your next home when you sell. If you’re using a home equity loan to “buy, build, or substantially improve” your property, the interest you pay may be tax deductible. This can have a big impact on the affordability of your home equity loan, so be sure to talk to your tax professional up front. Get all of our latest home-related stories—from mortgage rates to refinance tips—directly to your inbox once a week.

Costs of a Home Equity Loan

If you know how much you need to borrow and you want the security of a fixed interest rate, a home equity loan is a good choice. With a home equity loan, you borrow a set amount of money and pay it back over time, typically at a fixed interest rate. That fixed interest rate means your monthly payment will be constant over the term of your loan. In a rising rate environment, it may be easier to factor a fixed payment into your budget. Consolidating your credit cards or other loans into a single home equity loan can simplify your life and help you manage monthly bills.

You can save thousands of dollars over the life of your mortgage by getting multiple offers. The main difference between a home equity loan and a traditional mortgage is that you take out a home equity loan after buying and accumulating equity in the property. A mortgage is typically the lending tool that allows a buyer to purchase the property in the first place.

Pros and Cons of Home Equity Loans

The application process for home equity loans and HELOCs is less complicated than that for a mortgage, making it an attractive option. However, it’s important to shop around with different lenders to get the best rate. Experts strongly recommend having a repayment plan in place before borrowing with a home equity loan or line of credit. We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

It's possible to get more than one home equity loan on your house, but it can be difficult. You'll need to have enough equity in your home to support your primary mortgage and multiple additional loans. Additionally, many lenders won't want to be third in line for repayment if you run into financial troubles. The best lender for you can depend on your goals and your needs.

What percentage of your income should go towards your mortgage

“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced. Although Dave Ramsey has a large following of fervent fans, most financial experts question a considerable amount of the advice he gives.

Yourinterest ratewill be set when you borrow and should remain fixed for the life of the loan. Refinancing your home, getting a second mortgage, taking out a home equity loan, or getting a HELOC are common ways people use a home as collateral for home equity financing. But if you can’t repay the financing, you could lose your home and any equity you’ve built up. Your equity is the difference between what you owe on your mortgage and how much money you could get for your home if you sold it. High interest rates, financing fees, and other closing costs and credit costs can also make it very expensive to borrow money, even if you use your home as collateral.

Maurie Backman writes about current events affecting small businesses for The Ascent and The Motley Fool. Both a home equity loan and a HELOC let you borrow against your home. A home equity line of credit is a type of home equity loan that has a revolving line of credit.

In addition to however much you still owe on your first mortgage, taking out a home equity loan means you’ll have another large loan to repay at the same time. And like with a typical mortgage, your lender could seize your house if you fail to make your payments. If there’s any question that you’ll be able to manage two loans, don’t get a home equity loan. The interest rate on a home equity loan—although higher than that of a first mortgage—is much lower than that of credit cards and other consumer loans.

The amount above and beyond the mortgage payoff is issued in cash just like a personal loan. Unlike traditional mortgage loans, this does not have a set monthly payment with a term attached to it. It is more like a credit card than a traditional mortgage because it is revolving debt where you will need to make a minimum monthly payment. You can also pay down the loan and then draw out the money again to pay bills or to work on another project.

Comments

Post a Comment